หลักเกณฑ์การให้สิทธิและประโยชน์ |

||

|

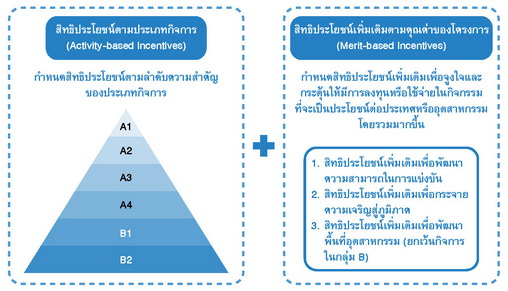

คณะกรรมการกำหนดรูปแบบของการให้สิทธิและประโยชน์เป็น 2 ประเภท ดังนี้ | |

|

||

สิทธิและประโยชน์ตามประเภทกิจการ |

||

| คณะกรรมการกำหนดสิทธิและประโยชน์ตามลำดับความสำคัญของประเภทกิจการ 2 กลุ่ม ดังนี้ | ||

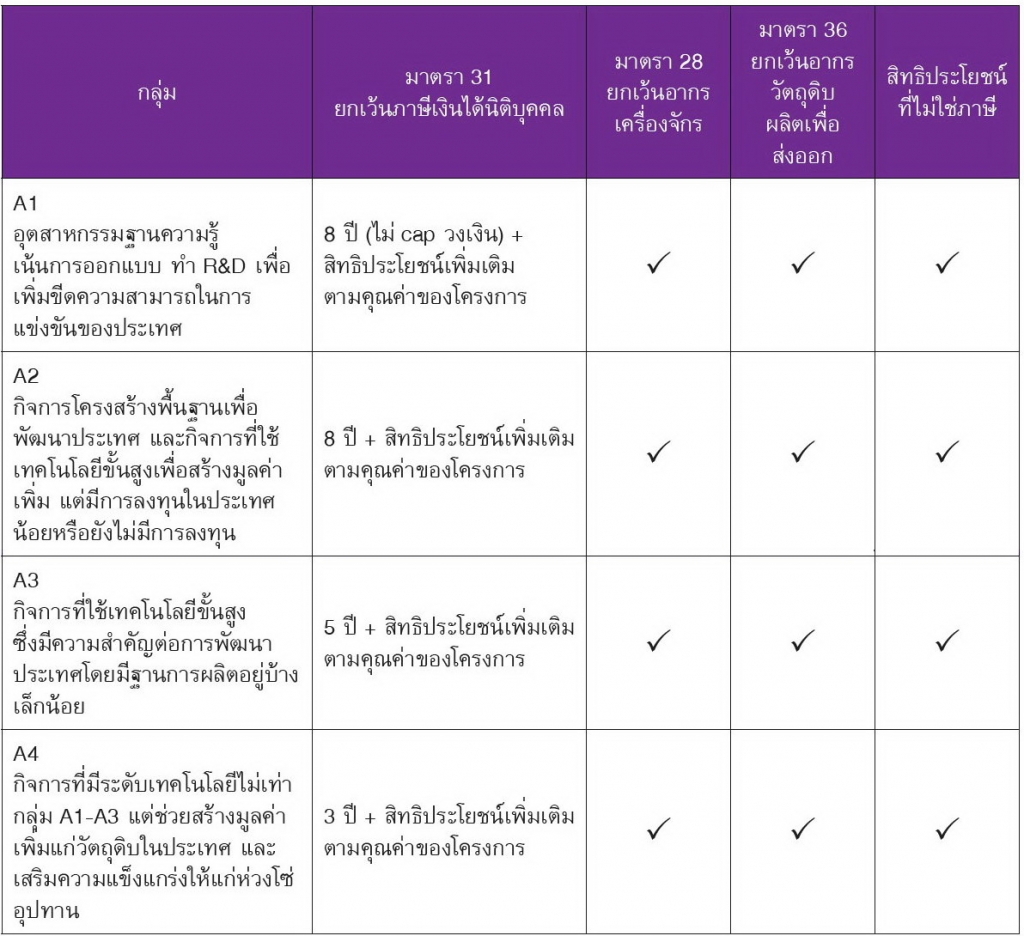

| กลุ่ม A | ||

| ตารางสรุปสิทธิประโยชน์ตามประเภทกิจการ กลุ่ม A | ||

|

||

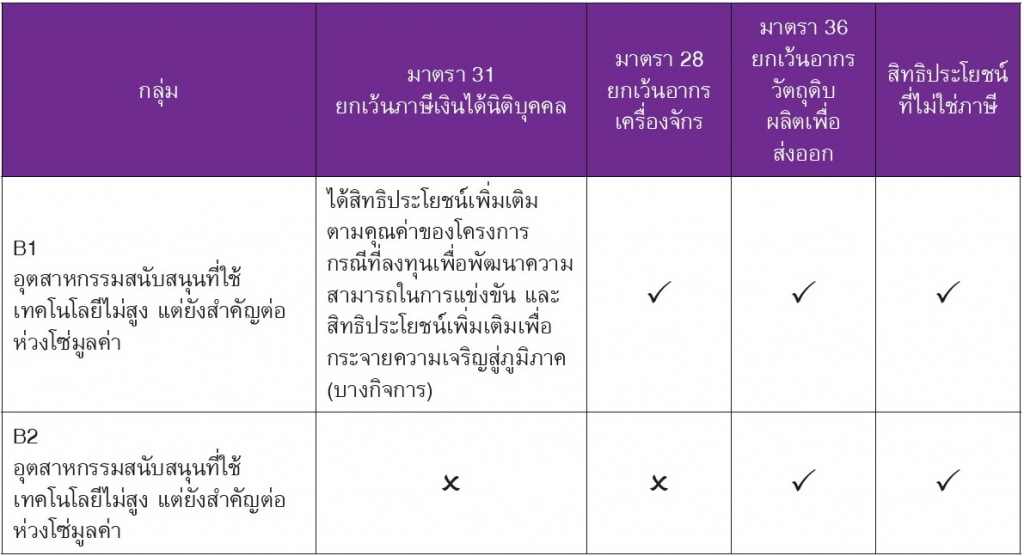

| กลุ่ม B | ||

| ตารางสรุปสิทธิประโยชน์ตามประเภทกิจการ กลุ่ม B | ||

|

||

Not Found

ขออภัยครับ ไม่มีข้อมูลส่วนนี้ ในภาษาที่ท่านเลือก !

Sorry, There is no information support your selected language !

Download และ ติดตั้งโปรแกรมอ่าน PDF

Download PDF ReaderSite map